This isn't about finding a "holy grail" setup. DOM trading is about understanding sequences of events that create high-probability scenarios. Think of it as learning to read micro-expressions in a poker game—the tell is there, but you need to know what you're looking for.

Absorption: The Wall That Holds

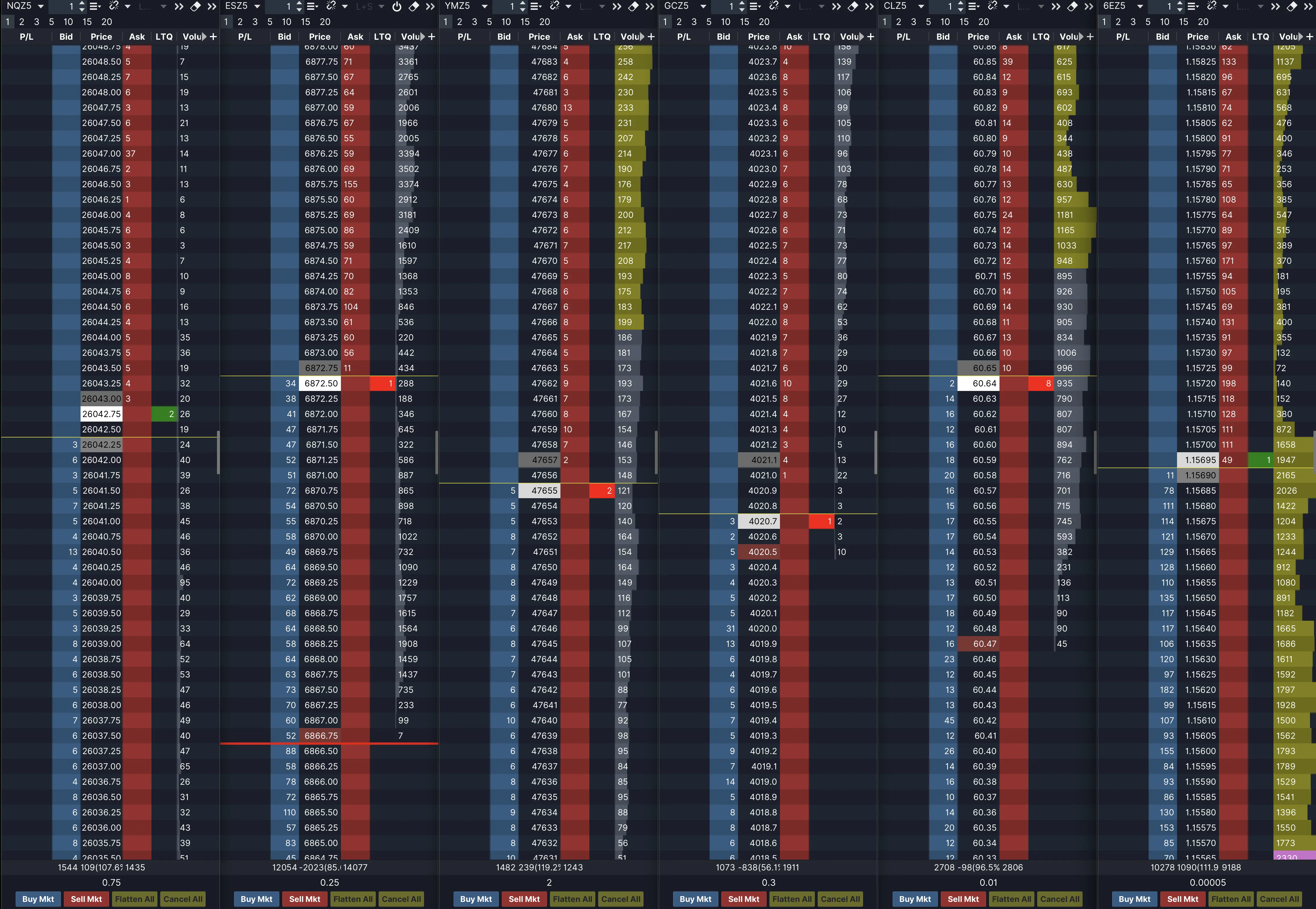

Absorption is the DOM pattern that separates amateurs from professionals. It occurs when large orders on a specific price level continuously accept incoming aggressive orders without the price moving through that level. You'll see hundreds of contracts being traded at 4550.00, but instead of the level breaking, it holds firm—and often reverses sharply.

How to spot it: Reset your DOM 2-3 ticks before a key level. Watch as market orders hammer into limit orders at that price. The volume traded increases dramatically, but the price refuses to move. The key identifier is this: if you see 800 contracts on the bid and aggressive sellers keep hitting it, but the price doesn't drop—that's absorption. Someone is using that level to accumulate a position.

The context matters: Absorption near previous day's high/low, value area boundaries, or session extremes carries more weight. After a spike into a level with large resting orders, absorption within 20 seconds signals exhaustion. The buying or selling can't overcome the passive liquidity, and the move is done.

Trading the setup: The risk is small because either the level holds or it doesn't. You don't need to give it much room. If absorption appears during RTH after a clean directional move, the probability of reversal increases significantly. Avoid trading absorption within 30 minutes of market open or before news releases—the noise-to-signal ratio is too high.

Stacking: Building the Pressure Cooker

Stacking is the accumulation of orders at specific price levels, creating visible "walls" in the order book. When you see bids or asks growing from 100 to 300 to 800 contracts at the same price, that's stacking. It represents committed interest—traders willing to defend or attack a price level.

Bid stacking vs Ask stacking: Heavy bid stacking suggests buyers are positioning for support, while ask stacking indicates sellers defending resistance. The critical observation is whether the stack is being consumed or reinforced. If aggressive orders hit the stack and it reloads immediately, the level is legitimate. If it pulls before contact, it was likely a bluff.

Delta confirmation: Watch your cumulative delta during stacking. When bid delta grows from -6 to -18 to -25, selling pressure is building. The price hasn't moved yet, but the coiled spring is tightening. Experienced traders enter before the breakout, not after—because by the time the stack breaks, the risk-reward has deteriorated.

Time element: Stacks that remain for 30+ seconds have more credibility than those appearing and disappearing in milliseconds. HFT algorithms create "flash stacks" to manipulate perception. Real institutional interest shows patience.

Pulling: The Vanishing Act

Pulling is when orders disappear from the DOM before being executed. You're watching a 500-contract bid at 4555.00, the price moves toward it, and suddenly those 500 contracts vanish. This tells you the order wasn't real interest—it was either spoofing or a trader who changed their mind.

Absorption-pull sequence: One of the highest-probability setups combines absorption and pulling. Price hits a level, gets absorbed (high volume, no movement), then on the 1-3 tick pullback, you see orders being pulled from the original direction. This confirms the move is reversing. The big player absorbed, and the weak hands who stacked behind them are now running.

Queue position games: Sometimes pulling happens because the trader realizes their queue position is too far back. They cancel and re-enter at a better price level. This creates micro-volatility as order sizes shift between ticks.

Red flag indicator: Heavy pulling without absorption often precedes fast moves. If you see large orders consistently being pulled as price approaches, it means there's no real interest at those levels—the market is likely to slice through them.

Spoofing: The Illegal Bluff

Spoofing is the practice of placing large orders with no intention of execution. A trader places 1,000+ contracts on the bid to create the illusion of strong support, encouraging other traders to buy. Once buying momentum builds, the spoofer pulls the order and sells into the demand they created.

Identification markers: Spoofing orders appear and disappear rapidly—usually within seconds. They're disproportionately large compared to normal market size. A typical ES session might see 100-300 contract orders regularly, but a spoofer places 2,000 contracts. The size is designed to intimidate and influence.

Market manipulation: While spoofing is illegal, it still happens, especially in less-regulated markets or during off-hours. The key is not to front-run these orders. If an order seems "too good to be true" as a signal, it probably is.

Defense strategy: Wait for execution confirmation. If a large order stays in place and starts getting filled, it's legitimate. If it pulls the moment price gets within 2-3 ticks, it was spoofing. Never base a trade solely on the presence of large orders—wait for the sequence to confirm.

Layering: Spoofing's Sophisticated Cousin

Layering takes spoofing to the next level by placing multiple false orders across several price levels. Instead of one fake 1,000-contract order, a trader places 200-300 contracts on five consecutive ticks, creating an illusion of massive liquidity.

Pattern recognition: Look for unusually uniform order sizes across multiple levels. Real market depth is messy—order sizes vary significantly. When you see perfectly symmetrical stacks (250, 250, 250, 250) across four ticks, that's algorithmic layering.

Direction clues: The layering typically appears opposite to the intended move. If someone wants to buy, they layer the ask side heavily to suppress price, then pull the layers and buy aggressively into the thin book they created.

Regulatory reality: Layering is a flagged behavior by exchange surveillance systems. It's considered market manipulation under CFTC regulations. As a retail trader, identifying layering helps you avoid being on the wrong side when these orders vanish.

Iceberg Orders: The Hidden Giant

Iceberg orders are large institutional orders where only a small portion is visible in the DOM. When you see a 50-contract order at 4560.00 that keeps refilling after execution—50 fills, then another 50 appears, then another—you're seeing an iceberg.

Detection technique: The order "regenerates" at the same price level. You'll see repeated executions without the order disappearing. Volume at that level is far higher than the visible size suggested. This is passive institutional accumulation or distribution.

True vs false absorption: Icebergs create genuine absorption. Unlike spoofing where orders pull, icebergs stay and absorb. The difference is commitment—the institution is willing to be filled. This makes iceberg levels strong support or resistance.

Trading implication: When you identify an iceberg during a pullback to a key level, the probability of reversal increases dramatically. The institution placing the iceberg has conviction, and their size can turn price. Front-running an iceberg after initial confirmation is a valid strategy—just ensure you see at least 2-3 refills first.

Sweeping: The Aggressive Hunter

Sweeping occurs when market orders aggressively take out multiple price levels in rapid succession. Instead of one tick moving, you see 3-5 ticks disappear instantly as someone "sweeps" available liquidity. The order book temporarily thins as layers get consumed.

Velocity indicator: Sweeps happen in under one second. The price ladder changes so fast your eye can barely track it. This indicates urgency—an institutional trader needs to fill a position NOW and doesn't care about slippage.

Liquidity vacuum: Post-sweep, the order book often shows voids—price levels with minimal orders. This creates volatility because there's nothing to stop the next move. If a sweep happens upward and creates a void below current price, expect fast movement if price reverses into that void.

Directional signal: Sweeps indicate momentum. A buy sweep through heavy ask resistance suggests strong bullish conviction. However, if the sweep doesn't continue and price stalls immediately after, it might be a failed breakout—setting up a fade trade.

Flipping: The Sentiment Shift

Flipping is the rapid reversal of order book dominance. The bid side shows 3:1 advantage, then within seconds, the ask side shows 3:1 advantage. This shift indicates changing market sentiment in real-time.

Trigger events: Flipping often occurs at key technical levels or after news. Watch for limit orders being pulled on one side while the opposite side reloads aggressively. The transition period—when the flip is happening—offers the best entry timing.

Confirmation sequence: A flip alone isn't a signal. Combine it with absorption or stacking. For example: heavy bid stacking, aggressive selling absorbs into the bids, then bids pull and asks stack—that's a confirmed flip with reversal potential.

False flips: During choppy, range-bound sessions, you'll see constant flipping without follow-through. Context matters. Flips at session extremes or near value area boundaries carry more weight than mid-range flips.

Reloading: The Determined Defense

Reloading occurs when executed orders are immediately replaced with equal or larger size at the same price. You see 100 contracts get filled at 4565.00, and instantly 101 or 120 contracts appear at 4565.00. This signals a committed defender.

Institutional fingerprint: Retail traders rarely reload—they get filled and reassess. Institutions reload because they have size to work and a price target in mind. Consistent reloading (3+ times) at a level confirms genuine interest.

Iceberg cousin: While similar to icebergs, reloading shows visible size changes. The trader isn't hiding their total size anymore—they're broadcasting commitment. This can be even more powerful than an iceberg because it psychologically impacts other market participants.

Probability assessment: When reloading appears after absorption at a key level with confluence (POC, VAH/VAL, previous session extreme), the setup reaches maximum probability. The institution is telling the market: "This is my line."

Liquidity Voids: The Danger Zones

Liquidity voids are price areas with extremely low or non-existent order depth. After sweeps or panic moves, the DOM shows huge gaps—prices with 5-20 contracts instead of normal 100-300 ranges.

Formation causes: Voids form when liquidity gets pulled or consumed. Post-news events, failed breakouts, or aggressive institutional entries create these dead zones. The order book needs time to repopulate.

Trading through voids: Price moves extremely fast through voids. If you're caught wrong-sided in a void, your stop might get significant slippage. Conversely, if you're right-sided, you get explosive moves with minimal resistance.

Strategic application: Identify voids before entering trades. If your stop-loss sits in a void, reconsider position size or entry. If your target is through a void, consider holding longer—price will likely reach it faster than expected.

Order Book Imbalance: The Pressure Gauge

Imbalance occurs when bid and ask volumes reach extreme ratios—3:1, 5:1, or higher. A 5:1 bid imbalance with 1,000+ contracts signals massive buying pressure. This pattern forecasts short-term direction.

Threshold significance: Minor imbalances (2:1, 100-500 contracts) appear constantly and mean little. Moderate imbalances (3:1, 500-1,000 contracts) warrant attention. Significant imbalances (5:1, 1,000+ contracts) are high-probability signals.

Duration factor: An imbalance lasting 5+ seconds is more significant than a 1-second flash. Sustained imbalance shows coordinated pressure, not algorithmic noise.

Reversal setup: Extreme imbalances near session extremes often precede reversals. When everyone is leaning one direction (reflected in DOM imbalance), contrarian setups become attractive—especially if combined with absorption.

Stop Hunt / Liquidity Grab: The Trap

Stop hunts occur when price deliberately spikes to trigger stop-loss orders clustered beyond key levels, then immediately reverses. In the DOM, you see a volume burst at the extreme, but no follow-through orders to support the new price.

Anatomy of a hunt: Price approaches a swing high or low. Suddenly, aggressive orders push through the level by 2-4 ticks. Volume spikes dramatically. Then—no continuation. Bids/asks on the other side remain thin or pull. Price snaps back within seconds.

DOM signature: The giveaway is the absence of supporting orders post-breakout. Real breakouts show committed orders stacking in the breakout direction. Stop hunts show voids—because the move was designed to hit stops, not establish new value.

Fade opportunity: Experienced traders fade stop hunts aggressively. The risk-reward is excellent: entry near the false extreme, stop just beyond, target back at the original level. Combine DOM confirmation (no stacking post-breakout) with volume profile (thin value area) for highest probability.

Momentum Ignition: The Manufactured Move

Momentum ignition is a manipulative pattern where traders create artificial price movement to trigger algorithmic responses and stop-losses. It involves three phases: stable accumulation with rising volume, explosive price move disproportionate to normal volatility, then return to original price at lower volume.

Phase identification: Watch for volume increasing 200-300% without corresponding price movement (phase one). Then sudden 10-15 tick moves in under 5 seconds (phase two). Finally, quick reversal with volume declining 50% (phase three).

Legal gray area: While momentum ignition isn't explicitly illegal like spoofing, it's ethically questionable and monitored by exchanges. As a trader, you want to avoid being the victim—which means not chasing explosive moves without DOM confirmation.

Protection strategy: If you see an explosive move without proper DOM buildup (no stacking, no absorption beforehand), assume manipulation until proven otherwise. Wait for the dust to settle. The best trades come after the fake move when price returns to fair value.

Ghost Liquidity: The Multi-Venue Illusion

Ghost liquidity refers to duplicate orders placed across multiple trading venues where only one is meant to fill. When execution occurs on one exchange, duplicates on others vanish within 100 milliseconds. This creates an illusion of deeper liquidity than actually exists.

Market reality: Research shows approximately 20% of displayed orders are duplicates, with 24% canceled immediately after fills on alternative venues. The true market depth is significantly thinner than DOM displays suggest.

Retail impact: You can't directly detect ghost liquidity on a single platform, but understanding it exists helps manage expectations. When large orders disappear "mysteriously" across the board, ghost liquidity is often the culprit—not manipulation.

Risk management: Because ghost liquidity inflates perceived depth, don't assume a level with 1,000 visible contracts will truly absorb 1,000 contracts. Build in buffers when calculating position size based on DOM liquidity.

Queue Position: The Invisible Race

Queue position refers to your place in the FIFO (first-in-first-out) order execution sequence at a specific price. The first order at 4570.00 gets filled first; the hundredth order might never fill if price moves away.

Positional awareness: Professional traders calculate their queue position constantly. If 500 contracts sit ahead of them at a price and only 200 typically trade there, they know they won't fill. They'll cancel and adjust.

Micro-modifications: You'll see order sizes at single prices fluctuating constantly as traders jockey for position. Someone places 5 contracts early to secure queue position, then increases to 50 once they're confident the level will trade.

Front-running dynamics: Small orders (1-5 contracts) appearing at key levels before larger orders stack behind them indicate queue position gaming. The small order captures priority, the large orders create the wall—both belong to the same sophisticated player.

Time Priority Exploitation: The HFT Advantage

Time priority means the first order at a price level gets filled first. HFT firms exploit this by placing small orders microseconds ahead of institutional flows, getting filled first, then canceling or flipping.

Pattern observation: Watch for tiny orders (1-2 contracts) appearing at obvious levels milliseconds before large orders. The tiny order is capturing time priority. Once the large order appears and validates the level, the small order gets filled at optimal prices.

Retail disadvantage: You can't compete with HFT on speed, but you can observe the pattern. When you see this behavior at a level, it confirms institutional interest is present—even if you can't get the perfect queue position yourself.

Adaptive strategy: Instead of trying to beat HFT to a price, wait for confirmation that the level is being defended (through reloading or absorption), then enter slightly worse but with higher probability.

Testing Zones: The Persistent Probe

Testing patterns occur when price repeatedly touches the same level with large DOM liquidity without breaking through. Each test partially fills the orders, but they reload. After 3-5 tests, the level either explodes through or reverses violently.

Test count significance: The first test is curiosity. The second test is challenge. The third test is determination. By the fourth test, energy is exhausted. The highest probability trades come after the third failed test—fading the tester or after the breakthrough when conviction finally wins.

Volume analysis: Compare volume on each successive test. Declining volume suggests weakening conviction—reversal likely. Increasing volume suggests building pressure—breakout imminent.

Context integration: Testing near session starts or value area extremes has higher significance. Mid-range testing during lunch hours often resolves with mean reversion rather than breakouts.

Confluence: Where Patterns Converge

No single DOM pattern guarantees success. The magic happens when multiple patterns align simultaneously. Absorption + pulling + imbalance at a key level with iceberg reloading—that's confluence. That's when probability shifts dramatically in your favor.

Layered confirmation: Start with the macro context (where are we in the session, what levels matter). Then watch for DOM patterns to confirm or reject your hypothesis. If absorption appears exactly where your market profile analysis predicted POC defense, the setup is validated.

Sequence thinking: Trading is pattern recognition, but patterns aren't shapes—they're sequences of events. Large resting liquidity (event 1) + price spike into that liquidity (event 2) + absorption (event 3) + pulling behind the level (event 4) = high-probability reversal sequence.

The DOM doesn't predict the future—it shows you the present with perfect clarity. Your job is interpreting what you see, understanding the story being told, and acting when the story you're reading has a high-probability ending. Master these patterns individually, then learn to read them in combination, and you'll see the market differently than 95% of traders ever will.

Frequently Asked Questions

What is the Depth of Market (DOM) and how is it different from a price chart?

The Depth of Market is a real-time display of all pending buy and sell orders at various price levels for a specific instrument. Unlike price charts that show historical price movements, DOM shows you the live order book—who wants to buy or sell, at what price, and how much volume they're offering. Think of it as seeing the market's intentions before they become price action. While charts tell you what happened, DOM shows you what participants are trying to make happen right now.

Do I need special software or subscription to access DOM data?

Most professional futures trading platforms include DOM functionality—platforms like NinjaTrader, Sierra Chart, TradingView (with certain brokers), and Jigsaw Trading provide DOM displays. However, access to real-time, detailed market depth data often requires a paid subscription or live trading account with specific data feeds. For futures traders, exchange fees for CME data (covering ES, NQ, etc.) are standard. Retail platforms may offer limited depth (5-10 levels) for free, while professional platforms show full depth with all price levels.

Which markets are best suited for DOM trading?

Futures markets are ideal for DOM trading because they're centralized exchanges with transparent order books. ES (S&P 500 E-mini), NQ (Nasdaq E-mini), and other liquid futures contracts provide the best DOM visibility. Forex is more challenging because it's decentralized—DOM data represents only your broker's liquidity, not the entire market. Stocks can work for DOM trading on highly liquid names, but futures remain the gold standard due to centralized order flow and high volume concentration.

How much capital do I need to start DOM trading?

DOM trading isn't capital-intensive in terms of minimum account size—you can start with $500-$1,000 for micro futures contracts (MES, MNQ). However, the real capital requirement is screen time and education. DOM patterns take hundreds of hours to recognize reliably. Start with micro contracts where each tick is $1.25 instead of $12.50, allowing you to learn without significant financial risk. Your capital should support 50-100 practice trades while maintaining proper risk management (never risk more than 1-2% per trade).

Can algorithms and HFT make DOM patterns unreliable?

Yes and no. HFT creates noise—spoofing, layering, ghost liquidity—but these behaviors themselves become recognizable patterns. The key is understanding which signals are reliable (absorption with reloading, iceberg fills) versus which are manipulation (massive orders that pull instantly). Retail traders can't compete with HFT on speed, but you can compete on pattern recognition and context. Algorithms react mechanically; humans adapt. Use DOM to confirm institutional behavior, not to front-run microsecond moves.

What's the difference between absorption and an iceberg order?

Both involve large passive liquidity, but the mechanics differ. Absorption is a pattern where incoming aggressive orders are continuously met by limit orders at a specific price without the price moving through that level—you see high volume traded but the price holds. Iceberg orders are specific order types where only a small portion of a large order is visible in the DOM—when that visible portion fills, it automatically replenishes. You can have absorption without icebergs (multiple different traders defending a level) and icebergs without absorption (if the iceberg isn't being hit).

How do I avoid being fooled by spoofing and layering?

The cardinal rule: never trade solely based on the presence of large orders—wait for execution confirmation. Legitimate orders stay in place and get filled; spoofed orders vanish before contact. Watch the sequence: if a 1,000-contract order appears, price approaches within 2-3 ticks, and the order suddenly disappears—that was spoofing. Real institutional orders show commitment through partial fills and reloading. If an order gets hit for 100 contracts and immediately replenishes, it's real. If it pulls before any execution, it was fake.